Analysis: There are two companies highly focused on DRAM and NAND production – Micron and SK hynix. Both are competing intensively in enterprise SSDs and high-bandwidth memory but came to their dual market focus in involved and indirect ways, via early sprawling business expansion, with mis-steps and inspired moves enroute.

One was blessed by Intel and one was cursed. Micron went into bed with Intel and the ill-fated Optane technology, which crashed and burned, while SK hynix bought troubled Intel’s SSD and NAND fab business, and went fast into the high-capacity SSD market, which took off and is flying high. It also stopped Western Digital merging with Kioxia, and then pushed early into the high-bandwidth memory (HBM) business and is now soaring upwards on Nvidia’s GPU memory coat tails.

Micron

Micron was started up in 1978 in Boise, Idaho by Ward Parkinson, Joe Parkinson, Dennis Wilson, and Doug Pitman as a semiconductor design operation. It started fabbing 65K DRAM chips in 1981 and IPO’d in 1984. A RISC CPU project came and went in the 1991-1992 period. Micron acquired the Netframe server business in 1997. It entered the PC business but exited that in 2002, and bought into the retail storage media business by buying Lexar in 2006

Micron entered the flash business in 2005 via a joint venture with Intel. It bought Numonyx, which made flash chips, in 2010, for $1.27 billion. It then developed its memory business by buying Elpida Memory in 2013, giving it an Apple iPhone and iPad memory supply business, also buying PC memory fabber Rexchip and Innotera Memories in 2016.

However, Micron entered into what was, with hindsight, a major mis-step in 2013 by joining Intel in the Optane 3D XPoint storage-class memory business and manufacturing the phase-change memory technology chips. It was even involved in producing its own branded QuantX 3D XPoint chips – but these went nowhere.

Despite Intel pouring millions of dollars into Optane, the technology failed to take off, with production volumes never growing large enough to lower the per-chip cost and so enable profitable manufacture. Eight years later, in March 2021, Micron cancelled the collaboration and walked away, stopping Optane chip production. Intel saw the writing was on the wall and canned its Optane business in mid-2022.

Ironically, Intel sold its NAND and SSD business to SK hynix in 2021, the same year that Micron up-ended the Optane collaboration. If only Micron had been in a position to buy that business it would now have to a stronger SSD market position.

Sanjay Mehrotra became Micron’s CEO in 2017 and it was he who pushed Optane out of Micron’s door. He also sold off the Lexar business to focus on DRAM and NAND.

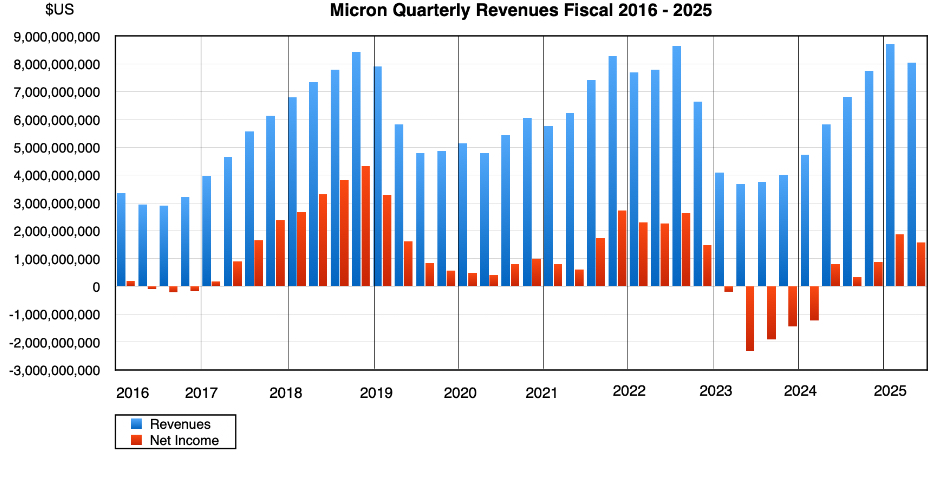

A look at Micron’s revenues and profits from 2016 to date show a pronounced shortage and glut, peak and trough pattern, characteristic of the DRAM and NAND markets:

During the Optane period from 2013 to 2021, Micron diverted production capacity and funding away from DRAM and NAND to Optane and, with hindsight again, we could say it would be a larger company now, revenue-wise, if had not done that.

SK hynix

SK hynix has a more recent history than Micron. It was founded as Hyundai Electronics Industries Co., Ltd. by Chung Ju-yung in 1983, as part of the Hyundai Group. It produced SRAM product in 1984 and DRAM in 1985. The company built a range of products including PCs, car radios, telephone switchboards, answering machines, cameras, mobile phones and pagers. It sprawled even more than the early Micron in a product sense.

Hyundai Electronics Industries bought disk drive maker Maxtor in 1993 and IPO’d in 1996. It bought LG Semiconductor in 1998. In 2000 and, in financial difficulties caused by DRAM price drops, it restructured with subsidiaries spun off. It rebranded its core business as Hynix Semiconductor in 2001 and then was itself spun out of the Hyundai Group.

More subsidiary divestitures followed in 2002 and 2004. The business then recovered but not for long as it defaulted on loans and went through a debt-for-equity swap. Its lenders put it up for sale in 2009 and Hynix partnered HP to productize Memristor technology, but that was a bust.

Hynix was fined for price-fixing in 2010, to add more trouble, and was eventually acquired in 2012 by SK Telecom for $3 billion. SK Telecom rebranded it as SK hynix with a focus on DRAM and NAND and it prospered and is prospering. SK hynix is headquartered in Icheon, South Korea.

The company was part of the Bain consortium which purchased a majority share in the financially troubled Toshiba Memory Systems NAND business in 2017. This business had a NAND fab joint venture with Western Digital and was rebranded as Kioxia.

SK hynix then bought Intel’s NAND business for $9 billion in 2021 in a multi-year deal; it completed earlier this year, and incorporated it in its Solidigm division, with NAND fabs in Dalian, China. This gave it an excellent position in the high-capacity SSD market and cemented its twin focus on DRAM and NAND.

A merger between Western Digital and Kioxia was suggested as a way forward for Kioxia in 2023 but eventually called off after SK hynix apparently blocked it. A combined Kioxia-WD business would have had a larger NAND market share than SK hynix, and a single NAND technology stack, lowering its costs.

SK hynix has two stacks: its own and Solidigm’s, and faced being relegated to number three in the market, with an 8.5 percent market share, behind Samsung and Kioxia-WD, both with about 33 percent.

Currently Samsung has a leading 36.9 percent share and SK hynix + Solidigm is in second place with 22.1 percent. These two are followed in declining order by Kioxia (12.4 percent), Micron (11.7 percent), Western Digital (now Sandisk and 11.6 percent) and others.

Solidigm took an early lead in high-capacity enterprise SSDs in 2024, with a 61.44 GB QLC drive and then a 122 TB drive in late 2024. This was well timed for the rapid rise in demand for fast access to masses of data needed for generative AI processing. Micron delivered its own 61.44 TB SSD later in 2024.

SK hynix started mass-producing high-bandwidth memory (HBM) in 2024 and has become the dominant supplier of this type of memory, needed for GPU servers, to Nvidia. As of 2025’s first quarter SK hynix holds 70 percent of the HBM market, with Micron and Samsung sharing the rest, proportions unknown. Micron says its HBM capacity is sold out for 2025 while Samsung’s latest HBM chips are being qualified.

Revenue-wise SK hynix and Micron were neck and neck in the DRAM/NAND market glut in mid-2023. But since then SK hynix has grown its revenues faster, led by HMB, with a widening gap between the two.

It seems unlikely that, absent SK hynix mis-steps, Micron will catch up. Its possibilities for catching up in the DRAM market could include getting early into the 3D DRAM business. Any NAND market catchup seems more likely to come from an acquisition; Sandisk anyone?

The two companies, Micron and SK hynix, have both been radically affected by Intel; Micron by the loss-making and jinxed Optane technology, and SK hynix by its market share-expanding Solidigm acquisition. Intel’s CEO at that time, Pat Gelsinger, said Intel should never have been in the memory business. Because it was, it helped hang an albatross around Micron’s neck and gave SK hynix a Solidigm shove upwards in the NAND business. Icheon benefited while Boise did not.