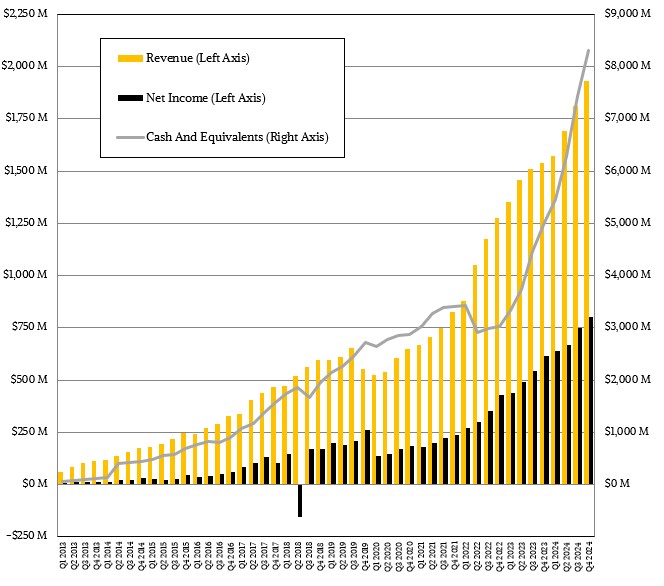

There has been no shortage of turmoil in the global economy thanks to war – trade and otherwise – and skirmish and terror of various kinds and severity. Despite all the uncertainty, business is business, and the hyperscalers and cloud builders need to upgrade their networks and the neoclouds need to find some sort of edge over each other, and so Arista Networks has broken through $2 billion in sales in a quarter for the first time, and it is set to one-up that in the second quarter of this year.

Imagine how good business might be without all of this uncertainty?

The 800 Gb/sec Ethernet upgrade cycle is underway in the datacenter, and Arista is getting its proportional and ever-embiggening share of that action for leaf and spine switches as well as for routing between datacenters. The “cloud titans” – what we call hyperscalers and cloud builders – bought a lot of gear in Q1 2025, and enterprises spent more on networking than Arista expected, and the company turned in its 20th quarter in a row of sequential growth, which is not an easy thing to do. That’s five years straight, and that is a very hard thing to do. (Amazon Web Services, as we pointed out recently, has done it for 76 quarters in a row, which is just amazing.)

It took Arista ten years from its founding to break through $2 billion in annual sales, and five years to break through $5 billion, and as we pointed out back in February, it is looking like Arista will cross through $10 billion in 2026 with relative ease. It is not hard, given the enormous fund that will be spent on AI networks and the desire to use Ethernet instead of InfiniBand, to imagine that within a few years Arista will have a $20 billion business, with a healthy mix if campus, datacenter, and edge use cases, and an AI business that is measured in the several billions of dollars annually.

In the current quarter, Arista’s top brass said the company was winning deals to retrofit campus and datacenter switching and making big inroads with datacenter routing based on merchant silicon, all across one EOS Linux network operating system and one telemetry and control plane. But Jayshree Ullal, chief executive officer at Arista, is careful about predicting the future in these uncertain times.

“We read the doom and gloom in the news, and we are not feeling it here,” Ullal told Wall Street analysts in a call going over the numbers for Q1. “I have never been a good soothsayer or forecaster of macro trends. Going back to my years at Cisco and now, recessions don’t give you a warning. They just happen. And at the moment, we do not see any warning of a recession. In fact, we are seeing the opposite. We are seeing a lot of demand, whether it is people pulling it in for tariffs or just the general excitement of Arista’s products. So unless things dramatically change with tariffs, which force a recession, Arista is really experiencing good momentum.”

Part of that is that when customers build a high bandwidth, back end network for an AI system, they then have to upgrade the front-end network that runs the infrastructure that feeds data from databases, storage, and applications into that AI system. You can’t have the latter on two lane gravel roads and feed smoothly into a six lane superhighway that is the former.

In the March quarter, Arista’s revenues rose by 27.6 percent to just a few million bucks above $2 billion, which also represented 3.9 percent sequential growth from a pretty good Q4 2024. Software subscriptions rose by 32.5 percent to $30.5 million, and are still a very small part of the business. This is due, in part, to the fact that many of Arista’s largest customers – namely Microsoft and Meta Platforms – are really “blue box” customers for a lot of the gear they buy from the company, meaning they run their respective SONiC and FBOSS network operating systems on Arista gear, and they pay a premium over whitebox hardware for certain use cases in the datacenter for the core network switches. These same customers as well as other cloud titans buy plenty of actual whitebox, barebones hardware.

This could change, of course, depending on the tariffs that the Trump administration imposes on gear manufactured outside of the United States. Rather than pay important duties on cheap foreign hardware, US companies may opt for gear made in Mexico (which is exempt for many kinds of IT gear manufacturing thanks to the USMCA trade agreement) or the United States and just pay the premium instead of a tariff.

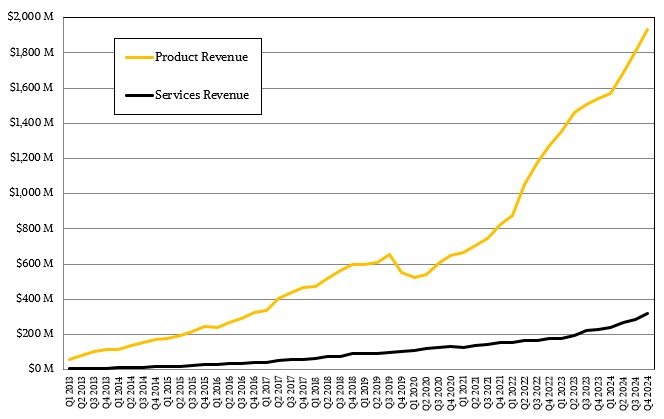

Product revenues in Q1 2025 rose by 27.4 percent to $1.69 billion, which was a 5.2 percent growth compared to Q4 2024. Services revenues rose by 28.8 percent year on year to $312.3 million, but that was a 3.1 percent decline from Q4 2024. Software subscriptions and services both fell sequentially, and it is not clear why.

Across all products and services, operating income was up 30.1 percent to $859 million and net income was up 27.6 percent to $814 million. Net income as a share of revenue was down a smidgen to 40.6 percent, compared to 41.3 percent in Q3 2024 and 41.5 percent in Q4 2023, but higher than the 39.4 percent in Q2 2024 and exactly the same level as reached back Q1 2024.

Ullal gave an update on the big four customers it has doing AI stuff.

“All of them are progressing well,” Ullal said on the call. “One of them is still new to us. They have been on InfiniBand for a long time, so they will be small. I would say two of them are heading towards 50,000 GPU deployments by end of the year, and I can be most certainly sure of 50,000 heading to 100,000. And then the other one is also in production. So I had talked about all four going into production, and three are already in production. The fourth one is well underway. So I think our back end number of $750 million – I am feeling good and feeling confident.”

Considering how much money is being spent on AI systems, this sounds like a low bar, but it is still early days for Ethernet to be used as a back end network for these clusters.

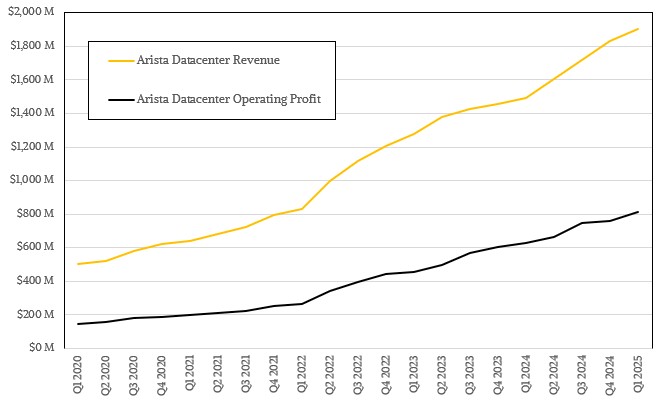

In terms of its datacenter business, we think that switching and routing products and services in the datacenter comprised $1.91 billion in sales in Q1 2025, up 27.6 percent, and operating profit attributable to this business was around $816 million, up 30.1 percent and comprising 42.8 percent of revenues. This is pretty good considering that Arista’s biggest customers drive the hardest bargains for steep discounts in the IT sector.

Looking ahead, Arista is telling Wall Street to expect $2.1 billion in sales in the second quarter, with gross margins of 63 percent and an operating margin of 46 percent. This is better on all fronts compared to Q1 2025. The company is not yet revising guidance for 2025, which was set at 17 percent growth for the full year to around $8.2 billion. It is not that Arista doesn’t have a sense of how it will go, but rather it does not want to revise guidance for all of 2025 until it knows what the tariff situation will be.

“Despite the macro uncertainty, we remain confident in the demand from our cloud enterprise and service provider customers,” Chantelle Breithaupt, the company’s chief financial officer, said on the call. “As is in the case of many other companies, the second half holds significant ambiguity relating to the tariff scenarios. Given these unknowns, our guidance for fiscal year 2025 currently remains unchanged despite the strong results and guidance we are reporting. We believe we can deliver results in the gross margin range of 60 percent to 62 percent even as we anticipate known possible tariff scenarios within Q3 and Q4. This is possible through a mix of supply chain optimization, tariff absorption and potential price increases if required.”

Given everything, this seems sensible.

And, so do stock buybacks, which us why Arista has just about finished buying up $1.2 billion in its stock and is now authorized by its board to spend another $1.5 billion in the years ahead. The company has another $100 million it will spend to expand its Santa Clara facilities in 2025.